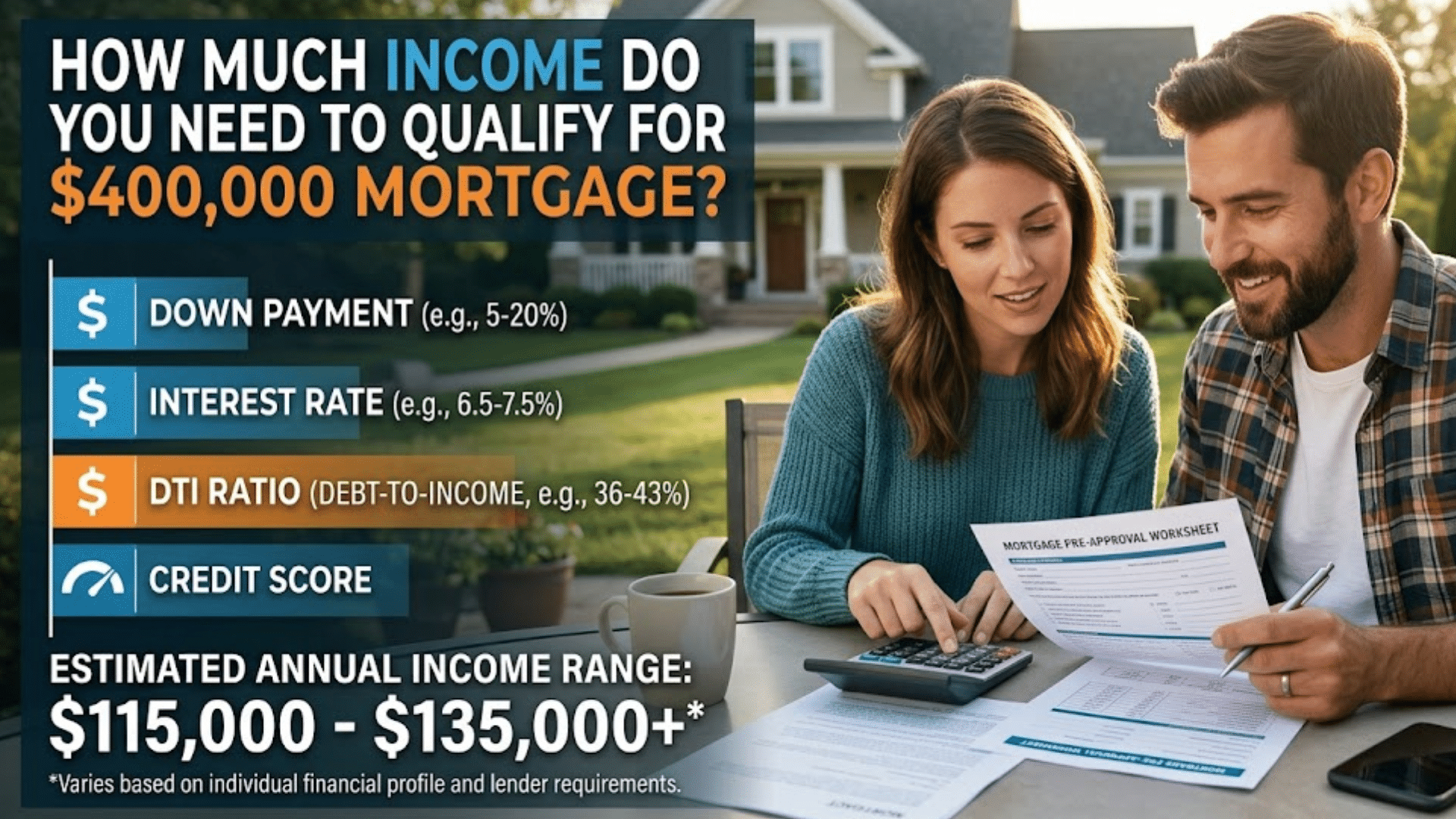

Buying a home is a major financial achievement, and most buyers are concerned about the income needed to qualify for a $400,000 mortgage. With home prices continuing to rise and interest rates constantly changing, understanding mortgage affordability has never been more important. While many buyers may be able to afford a $400,000 mortgage, qualifying for one depends on more than just your salary. Lenders consider several factors, including your income, debt-to-income (DTI) ratio, credit score, and current interest rates, before approving a loan.

Many prospective buyers assume that a fixed income is required, but in reality, the amount varies widely from one borrower to another. A purchaser with minimal debt and a strong credit profile may qualify with a lower income, whereas someone with existing student loans or credit card debt may need to earn more. Additionally, loan types such as conventional or VA mortgages have different eligibility requirements that affect the income needed.

In this article, we will explain how lenders calculate income eligibility and determine monthly payments, as well as the factors such as debt and down payments that affect affordability. By the end, you will have a clear understanding of whether a $400,000 mortgage fits your financial profile and what steps you can take to improve your chances of approval.

Key Factors Lenders Use to Determine Mortgage Eligibility

Before determining how much income you need, it’s important to understand how lenders evaluate borrowers.

Gross Monthly Income

Lenders look at your gross income, meaning your earnings before taxes and deductions. This includes salary, hourly wages, bonuses, commissions, and consistent secondary income. Self-employed borrowers may need to provide two years of tax returns to verify stable earnings.

Debt-to-Income (DTI) Ratio

DTI is one of the most critical factors in mortgage approval. It compares your monthly debt obligations to your gross monthly income.

- Front-end DTI: Percentage of income spent on housing costs

- Back-end DTI: Percentage spent on all debts, including housing

Most lenders prefer a back-end DTI of 36% or lower, though some loan programs allow up to 43% or even 50% in special cases.

Credit Score

Your credit score impacts both approval and interest rates. Higher scores typically result in lower interest rates, which can significantly reduce the income needed to qualify.

Down Payment

A larger down payment lowers the loan amount and monthly payment, improving affordability and reducing income requirements.

Estimated Monthly Payment on a $400,000 Mortgage

Your required income depends heavily on your monthly mortgage payment.

Loan Amount vs Purchase Price

- 5% down payment: Loan amount ≈ $380,000

- 10% down payment: Loan amount ≈ $360,000

- 20% down payment: Loan amount ≈ $320,000

Monthly Payment Breakdown

A typical mortgage payment includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- Private Mortgage Insurance (PMI), if applicable

At a 6.5% interest rate, estimated monthly costs might look like:

- Principal & interest: $2,200–$2,500

- Taxes & insurance: $400–$600

- PMI (if applicable): $100–$250

- Estimated total monthly payment: $2,700–$3,200

How Much Income Do You Need for a $400,000 Mortgage?

Lenders generally apply DTI rules to determine income eligibility.

Income Required Based on DTI Guidelines

Using the 28% housing rule:

- Monthly housing cost of $3,000 ÷ 0.28

- Required gross monthly income ≈ $10,700

- Annual income ≈ $128,000

Using a 36% total DTI:

- $3,000 ÷ 0.36

- Monthly income ≈ $8,300

- Annual income ≈ $100,000

Using maximum 43% DTI:

- $3,000 ÷ 0.43

- Monthly income ≈ $7,000

- Annual income ≈ $84,000

Estimated Annual Income Range

Most buyers need an income between $85,000 and $130,000 per year, depending on debt, credit score, and down payment.

Single vs Dual-Income Households

Dual-income households often qualify more easily since combined income lowers the DTI ratio, even if one borrower has existing debt.

Income Requirements by Loan Type

Conventional Loan

- Typically requires higher credit scores (620+)

- DTI usually capped at 36–43%

- Income needed: $95,000–$130,000

FHA Loan

- Allows lower credit scores and higher DTI

- Mortgage insurance increases monthly cost

- Income needed: $85,000–$115,000

VA Loan

- No down payment required

- No PMI, but residual income rules apply

- Income varies by household size and region

Jumbo Loan (If Applicable)

- Higher income and cash reserve requirements

- Often requires excellent credit

- Income may exceed $150,000+

Tips for Affording a $400K Mortgage

Affording a $400,000 mortgage requires smart planning and disciplined financial habits, but with the right approach, it can be well within reach. One of the most effective strategies is to reduce existing debt before applying. Paying off credit cards, personal loans, or even a car loan can significantly improve your debt-to-income (DTI) ratio and help you qualify for better loan terms.

Another key strategy is to save for a larger down payment. Putting down 20% not only lowers your loan amount but also eliminates private mortgage insurance (PMI), reducing your monthly payment. Equally important is improving your credit score. Even a small increase can help you secure a lower interest rate, which can save thousands of dollars over the life of the loan.

It’s also wise to shop around for lenders. Comparing interest rates, fees, and loan programs can uncover more affordable options. Additionally, consider locking in your rate when market conditions are favorable.

Finally, create a realistic household budget that accounts for property taxes, insurance, maintenance, and emergency savings. Planning beyond the mortgage payment ensures long-term affordability and financial peace of mind.

How Reliance Financial Helps in Qualifying a $400,000 Mortgage?

Personalized Mortgage Guidance

Reliance Financial offers one-on-one support throughout the mortgage journey. Their expert loan officers walk you through the entire process from assessing your financial profile to matching you with the right loan program. This level of guidance is especially useful if you’re unsure how your income, credit score, or debts affect your ability to qualify for a larger mortgage.

Competitive Rates and Loan Options

They provide access to competitive interest rates and a variety of mortgage loan types (such as conventional, fixed-rate, and government-backed options). Securing a favorable rate can lower your monthly payments, effectively reducing the income you need to qualify for a $400,000 loan.

Pre-Qualification and Pre-Approval

Reliance Financial allows you to get pre-qualified or pre-approved quickly with their online application tools. A pre-approval gives you a clear picture of how much you can borrow based on your income and credit, empowering you to shop for homes within your budget with confidence.

Educational Resources

Their website includes helpful guides on how to get preapproved, understanding private mortgage insurance (PMI), and qualifying for different loan programs, which can help you improve your eligibility for a larger mortgage.

Smooth & Supportive Process

Clients commonly report that Reliance Financial’s team provides transparent communication, fast turn-arounds, and responsive service, all of which can reduce stress and uncertainty when qualifying for a significant mortgage like $400,000.

Final Thoughts: Is a $400,000 Mortgage Affordable for You?

Qualifying for a $400,000 mortgage typically requires an annual income between $85,000 and $130,000, depending on your financial profile. While income is crucial, factors like debt, credit score, down payment, and loan type play an equally important role. Understanding these variables allows you to plan more effectively and avoid overextending your finances. Before committing, review your budget carefully and consult with a mortgage professional to determine the most comfortable and sustainable path to homeownership.

Frequently Asked Questions

Q1: What salary do I need to afford a $400,000 house?

Most buyers need a salary between $85,000 and $130,000 annually, depending on debts and interest rates.

Q2: Can I qualify with less income if I have no debt?

Yes, having little or no debt significantly improves your DTI and approval chances.

Q3: Does a higher credit score reduce income requirements?

Yes, higher credit scores often qualify for lower interest rates, reducing monthly payments.

Q4: How much down payment is ideal for a $400,000 mortgage?

A 20% down payment is ideal, but many programs allow less.

Q5: Can self-employed borrowers qualify for a $400,000 mortgage?

Yes, with consistent income documentation and stable earnings history.