Buying a home is likely the biggest investment most people will make in their lifetime. After weeks of searching, paperwork, and discussions with a lender, getting mortgage approval can feel like the final step before finally getting the keys. However, many first-time buyers are surprised to learn that approval doesn’t always mean the process is finished.

In reality, a deal can still fall through even after approval, sometimes just days before closing. That’s because lenders continue to review your financial situation, employment, credit, and even details about the property itself until the loan is fully finalized.

Knowing more about mortgage approval conditions and deal breakers can help you to prevent future problems and increase the odds of a successful closing.

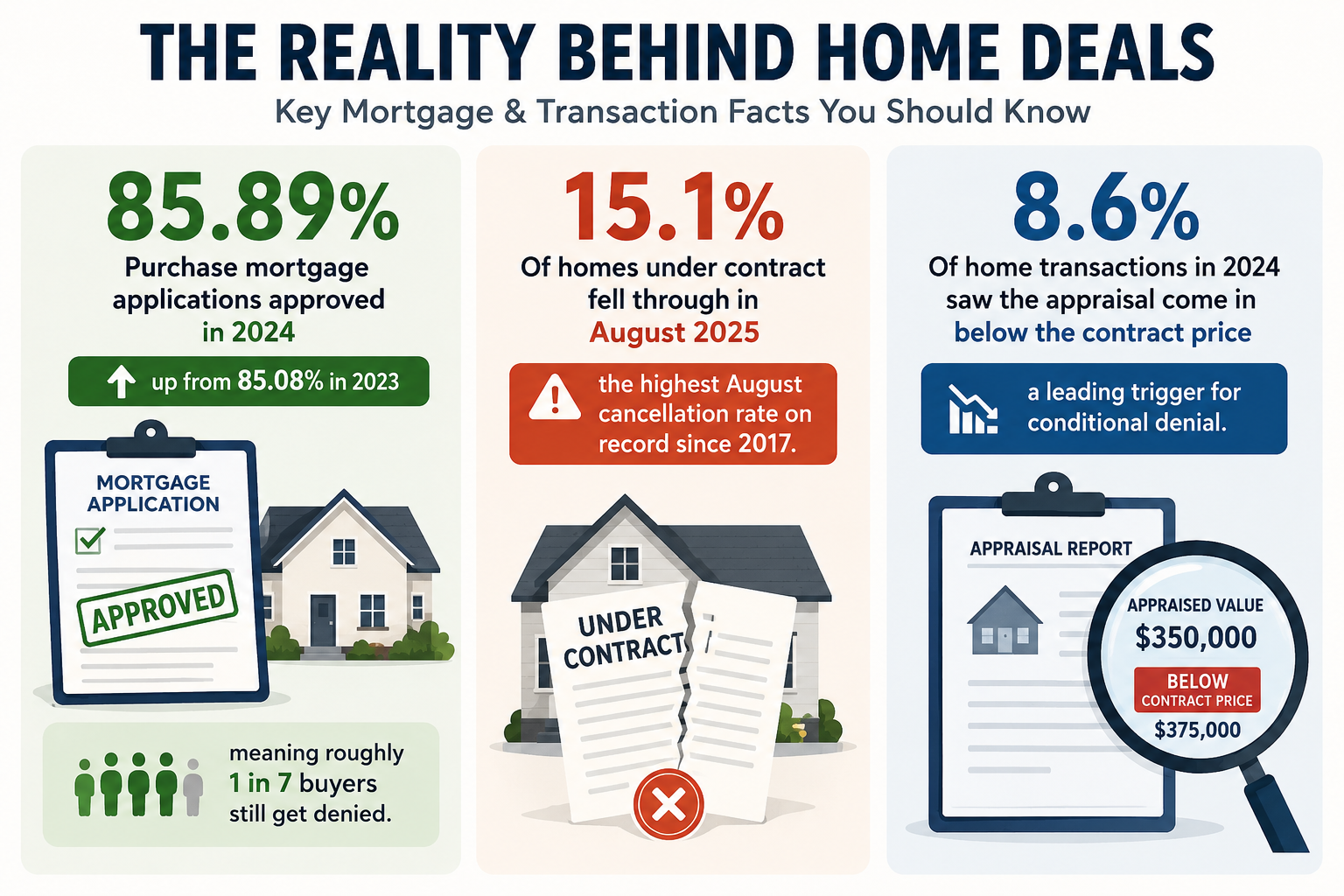

Some Facts that You Need to Know

Here’s the image that shows the interesting things that you need to know. The source of these data from Chase, Fortune, and Homebuyer.

What Is Conditional Mortgage Approval?

Getting pre-approved for a mortgage means the bank has reviewed your financial situation and is willing to offer you a loan, as long as you meet certain conditions.

At this time, the bank has already considered:

- Monthly income and employment history

- Credit score and behavior

- DTI (Debt-to-income) ratio

- Personal savings and down-payment money.

Based on these, the bank has deemed you potentially eligible for the mortgage loan. The final determination, however, can only be made once more documents have been evaluated, and a full underwriting has been completed.

Usual requirements would be:

- Recent bank statements

- Updated pay stubs

- Proof of employment

- Appraisal report of property

- Home Insurance Policy

- Tax Returns

Key Difference

| Phase | Meaning |

| Pre-qualification | Rough estimate based on self-assessment |

| Pre-approval | Lender’s initial analysis of finances and creditworthiness |

| Conditional approval | Loan approved, subject to fulfillment of certain conditions |

| Final approval | Loan approved and ready to close |

Conditional approval is a great move forward, but not a guarantee.

Why Some Mortgages Fall Through After Conditional Approval

Even after conditional approval, there are still many reasons that will lead to lenders rejecting the mortgage application.

Job Changes

One of the key factors in getting approved for a mortgage is having a stable source of income. Because of this, any change in employment could affect your approval.

Some examples of things that could happen include:

- Changing the current job

- Resigning from work

- Cutting back on working hours

- Becoming a freelancer

Even though moving to a higher-paying job may seem like a positive change, lenders may delay the process or even deny approval due to concerns about income stability. For example, if an applicant switches from a salaried position to commission-based work, it can be seen as higher risk. As a result, lenders may require additional time to reassess the situation and verify income consistency.

Credit Score Changes

Another reason why some mortgages fall through after conditional approval is changes in credit score.

Some common mistakes include:

- Opening new credit accounts

- Applying for a car or personal loans

- Increasing balance on credit cards

- Missing payments

Most people tend to make the mistake of buying items such as furniture or appliances before closing. This increases debt levels, reducing borrowing power.

Any minor changes in credit score or debt-to-income ratio may have negative effects on the approval process.

Also Read: How To Improve Your Credit Score For Better Mortgage Rates

Property Issues

The property itself must fulfill the criteria set by lenders since it is used as collateral.

Issues that may arise:

- Appraisal too low

- Structural issues

- Disputes over title

- Insurance issues

- Property in bad condition

A low appraisal will force the lender to cut down the amount of the loan, forcing buyers to renegotiate.

Inspection problems may also prevent lenders from financing.

Documentation Issues

Almost every lender relies heavily on proper documentation for mortgage approval. So, ignoring documentation can create problems.

Potential red flags include:

- Big bank deposits without explanation

- Lack of tax records

- Inconsistent income information

- Hidden debts

- Errors in application data

An example would be an issue where big bank deposits without an explanation may raise suspicion. Lenders may treat this as a financial risk.

Market or Lending Trends

In some cases, external factors influence the process.

- Increasing interest rates may make it difficult to qualify

- Lending trends may become more stringent

- Market uncertainty may result in stricter lending standards

Such changes could also affect applicants even after conditional approval.

Red Flags That May Raise Concern before Loan Approval

Lenders closely examine the financial conduct of their clients. Some red flags that would raise concern include:

- Obtaining new credit cards or loans

- Late or missed payments

- Unexplained large cash deposits

- Overdrafts

- Gambling activities

- Making big purchases before loan approval

- Dipping into savings

- Applying for several loans

Timeline from Conditional Approval to Closing

It will help you avoid any misunderstandings:

- Loan application submitted

- Initial review performed

- Conditional approval obtained

- Property appraised

- Additional documentation requested

- Re-verification of employment and credit history

- Final underwriting performed

- “Clear to close” obtained

- Closing documents signed

Your mortgage loan cannot be considered finalized until the “clear to close” is obtained.

How to Safeguard Your Mortgage Approval

Mortgage failure is usually avoidable. Here are some ways borrowers can safeguard their approval:

Maintain Financial Stability

Borrowers should never make any significant changes to their finances:

- Do not apply for a loan or a credit card

- Do not get a car loan

- Make sure credit balances are low

Stability shows reduced risks to lenders.

Maintain Employment Stability

Do not change your employment status before the closing date. In case you must, let the lender know right away.

Changing employment status may result in income evaluation and even underwriting delay.

Be Prompt with Documentations

Any delay in providing documents will negatively affect the mortgage approval process.

- Provide documentation as soon as possible

- Make sure all the information provided is accurate

Always be prompt in responding to the lender’s requests.

Be Honest

Transparency is always encouraged. Be honest about:

- Large deposits

- Any debt

- Any changes made to your financial status

Transparency is preferred in underwriting.

Have Additional Funds at Hand

Closing costs might put pressure on your financial situation. Extra money would help with closing costs.

What Would Happen in Case of Denial of the Mortgage?

It can be very upsetting, yet not necessarily final.

First, ask the lender for the reason, since many issues can be resolved easily, such as missing documents or a poor credit history.

Some of the solutions might be:

- Reducing debts

- Improving your credit rating

- Making a larger down payment

- Getting a co-signer

- Trying to get approval from a different bank

Different financial institutions have different approval requirements.

Conclusion

A conditional mortgage approval is an important step, but it doesn’t mean the mortgage has been finalized yet. Your finances, credit score, employment status, and details about the property will continue to be reviewed until the lender gives final approval and the deal closes.

In many cases, mortgages are denied for issues that are actually avoidable, such as taking on new debt, changing jobs, or failing to submit required documents. Because lending involves financial risk, banks follow a strict review process to protect themselves.

To reach the closing stage smoothly, it’s important to keep your finances stable, avoid making major credit changes, and respond quickly to any lender requests.

In the end, Reliance Financial suggest that the best approach is simple: manage your finances carefully until the deal is closed, since nothing is final until you have the keys in hand.

FAQs

Is it possible to deny a mortgage after conditional approval?

Yes, it is possible since the mortgage can be denied after conditional approval for various reasons, such as employment change, a decrease in credit scores, problems with the property, or documents.

What is the meaning of conditional mortgage approval?

Conditional mortgage approval means that the bank is ready to give the loan but requires the applicant to fulfill some requirements before signing the agreement.

Does the bank do a credit check before closing the deal?

Yes, banks usually conduct an additional credit check to see whether the client has taken a loan, missed some payments, and what their current credit score is.

What actions should I avoid after mortgage approval?

You need to avoid opening new accounts, changing employment, buying expensive things, and paying more on credit cards since this can negatively impact the debt-to-income ratio.

How long is conditional mortgage approval valid?

It is usually valid until the closing takes place and lasts from 30 to 60 days, depending on the lender’s policies.

Will job change influence mortgage approval

Job change can negatively impact the process since lenders prefer applicants with stable employment and may require re-verification even when it comes to better positions.

What will happen in case I miss a document after conditional approval?

The absence of documents may postpone or even endanger the process of mortgage approval. The lender can stop processing the application for the time being until all necessary paperwork is received and confirmed.

Why does the lender need to check everything again before closing?

The purpose of additional verification before closing is to make sure that there were no significant changes to the borrower’s finances. They include credit score, employment, income, and debt.

Can new debt affect mortgage approval?

New debt makes it harder for a borrower to obtain a mortgage because it affects his/her debt-to-income ratio. Any type of debt will be considered during the underwriting process.

Does conditional approval mean guaranteed loan approval?

Conditional approval does not mean guaranteed loan approval. Conditional means that approval will depend on certain conditions. The loan will be approved only when all conditions are fulfilled.

What is the most important reason for mortgage deal cancellation?

The most important reason for the cancellation of mortgage deals is changes in finances. New employment, lower credit score, or new debt will affect the approval decision negatively.