Homeownership is considered one of the most significant decisions an American citizen has to make. In view of the evolution of the American housing market due to increasing prices on property, fluctuations in mortgage rates, and economic instability, adequate planning in order to buy a house by 2027 is highly important. Proper financial planning will allow people to obtain good mortgage rates and prevent any financial difficulties.

While trying to buy a house, many Americans focus on saving enough money for a down payment but neglect other financial aspects such as credit score, debt levels, income, and savings. If you start preparing yourself financially in advance, you will have time to achieve a perfect financial condition to acquire your home.

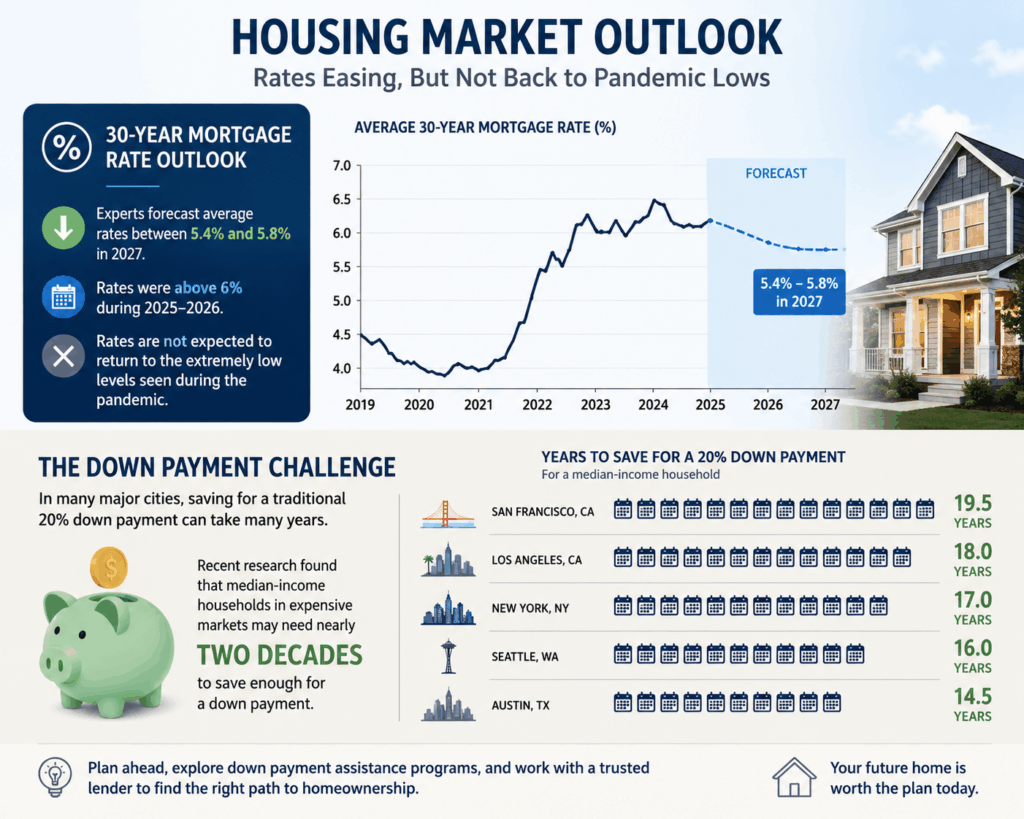

Market Insights on Finances to Buy A House in the U.S. in 2027

Here’s the stats which shows the overview of finances to buy a house. Sources of this information is from mortgage-info, and nypost:

Tips to prepare finances to buy a house in 2027

Here’s the top tips which you can follow to prepare finances so that you can buy a house in 2027, and achieve you milestone of buying home:

Review Your Current Financial Situation

The first step to consider when thinking about purchasing property entails becoming acquainted with one’s current financial situation. It is necessary to evaluate one’s income, expenditure, debts, and financial behavior prior to setting any financial targets or identifying mortgages.

Here’s the some examples of information that needs analysis include:

- Monthly salary

- Expenditures

- Loans

- Savings

- Investments

- Credit card debt

- Emergency funds

Knowing these factors allows one to understand whether one can afford to purchase a property in 2027. There are many individuals who misjudge their economic situation and face difficulties repaying their debts afterward. Financial preparation may allow one to avoid such issues.

In addition, one must also focus on one’s spending habits. Going out to eat frequently, purchasing unnecessary products, and numerous paid subscriptions may negatively impact one’s savings strategy. Cutting back on such expenses enables one to save more money.

Knowledge of finance is essential to make the right decision.

Improve Your Credit Score

Another significant factor that mortgage lenders consider when assessing the creditworthiness of a borrower is his/her credit score. The lender considers the credit score of a borrower while analyzing his/her ability to meet the financial obligations.

A good credit score often results in:

- Lower interest rates for mortgages

- Better loan terms

- Affordable monthly payments

- Approval for loans

In the case of conventional mortgages in the USA, the lender prefers the minimum credit score of 620, but the person who has a credit score above 740 will receive better interest rates.

Getting good credit scores demands continuous effort. Some of the steps you should take to improve your credit scores are:

- Timely payment of bills

- Reducing the credit card balance

- No missed payments

- Having a low credit utilization ratio

- Reviewing your credit report periodically

- Reporting any errors in the credit report

Payment defaults and debts will damage your credit score. As gaining good credit scores takes time, people who are thinking about buying houses in 2027 must prepare themselves today.

Also Read: Can I Pay My Mortgage With A Credit Card?

Save for a Down Payment

The second problem associated with purchasing a house is whether one has enough savings to cover the down payment. This will depend on the type mortgage loan for down payment that one prefers and the value of the house.

Down payments in the USA are generally set at:

- 3%-5% for certain first-time home buyer schemes

- 10%-20% for normal mortgage schemes

- 20% or more to avoid the cost of PMI

Making a larger percentage of down payments will help in many ways. For instance, individuals who make huge down payments are believed to enjoy more favorable mortgage schemes and lower monthly repayments when they obtain mortgages. They will save money since they will not incur the cost of obtaining insurance on top of other expenses.

Some ways of saving more quickly for the down payment may include:

- Starting a savings account for house expenses

- Automatically saving a fixed amount every month

- Curtailing unnecessary expenditure

- Saving extra money like bonuses and tax refund money

- Working additional hours or taking part-time jobs

Saving goals must be practical. For example, if one wants to buy a $400,000 home in 2027 and the down payment is 20%, then one will need to save about $80,000.

Savings should always be done as soon as possible.

Build an Emergency Fund

In general, the majority of the future homeowners consider their down payments but not their emergency funds. However, there are several unforeseen expenses associated with being a homeowner that cannot be experienced while renting a residence.

Such expenses may include:

- Roof repair expenses

- Pipe problems

- Heating Ventilation Air Conditioning system installation

- Appliance malfunctioning

- Maintenance charges

- Medical emergencies

- Low income

According to the financial advice, one needs to keep between three and six months’ expenses in their emergency funds. Due to the unpredictability of maintenance costs, one should always set aside more money compared to the financial advice.

It is important to save some money for unforeseen events after purchasing a house. Without any emergency funds, borrowing money due to the unforeseen maintenance expenses cannot be avoided.

Besides, the mortgage lenders will be assured that you are capable of taking care of the house as a responsible homeowner.

Reduce Existing Debt

This is another key element of preparing for homeownership. This involves the handling of debt. The lending institution will look at one’s debt to income ratio (DTI) which refers to the percentage of one’s earnings being used to service the debt.

This could result in:

- Making it difficult for one to get approval

- Reducing the amount of money one can borrow

- Increasing mortgage interest rates

- Financial stress after buying

The type of debts that affect one’s capability to qualify for a home loan include:

- Credit card debts

- Auto loans

- Student loans

- Personal loans

One is advised to settle debts before applying for a mortgage because it makes it easy to get a loan. In other words, one is supposed to clear debts but not in the form of new loans.

Among the strategies for clearing one’s debts include:

- Planning how to clear debts

- Consolidation of debts with high-interest rate

- Make larger monthly payments

- Avoid impulsive purchase

- Control credit card spending

Types of Mortgage Options

Here’s the table about types of mortgage options:

| Types of Mortgages | Description | Advantages | Beneficiaries |

| Conventional Mortgage | Government-insured mortgages available to applicants who have strong credit records and financial stability. | Competitive pricing and flexible repayment terms. | Persons with favorable credit history. |

| FHA Mortgage | Government-sponsored mortgages aimed at promoting homeownership among citizens. | Low down payment requirements and flexible credit standards. | Couples planning to own their first home. |

| VA Mortgage | Home mortgages available to qualified military veterans. | No down payments required and favorable interest rates. | VA borrowers and military families. |

| USDA Mortgage | Home mortgages that help in purchasing homes within specified rural areas. | Affordable financing for purchasing homes. | Citizens buying homes in rural locations. |

The Real Costs of Owning a House

Owning a house is not only about paying your monthly mortgage repayment. Most first-time homeowners fail to recognize the real cost of owning a house.

Other costs that come along with owning a house are:

- Property tax

- House insurance

- HOA fees

- Utility bills

- Maintenance fee

- Repairs

- Lawn care

- Closing cost

It is vital that you factor in all these extra costs while preparing your budget. It would be better if you were able to determine the total cost of housing before thinking of purchasing a house.

With a mortgage calculator, you can determine these costs:

- Principal and interest

- Property taxes

- Insurances

- Total monthly cost

Monitor the Housing Market

The housing market in America is always changing according to the economy, mortgage rates, and demand for houses. For anyone planning to buy houses in 2027, there is a need to consider trends in the housing market early enough.

There are certain factors that one needs to consider such as:

- Mortgage rate trends

- Prices of real estate in different locations

- Availability of housing in the area

- Economic predictions

- The population in different areas

This will enable individuals to get to know which areas are affordable and profitable in the future.

How To Earn More Money?

With more earnings, you will be in better financial shape and have an easy time securing mortgages.

Other sources of income may include:

- Freelance work

- Homemade business

- Consultancy

- Other investments

- Investment Income

- Professional Success

Having more sources of income will make it easier to accumulate savings and lower the costs of purchasing properties.

Income stability is always favored when looking for mortgage services. Income stability will enable loan applications to be successful and also borrow larger amounts.

More income, even if small, will be useful.

Avoid Major Financial Changes Before Buying

It is important to mention that financial stability is one of the key factors for the mortgage application process. Therefore, carrying out any financial activities before applying for the mortgage may be considered as a negative factor.

In general, when preparing for a home purchase, it is necessary to avoid:

- Getting a loan to buy a car

- Opening new accounts

- Receiving any personal loans

- Purchasing something expensive

- Changing jobs often

- Missing payments for bills

Bankers and mortgage lenders will be pleased to see such behavior from potential borrowers.

Conclusion

Getting finances ready for acquiring a home in 2027 entails a lot of deliberation and hard work. Those who will start early will get benefits in terms of better credit score, ability to pay off debts, save money, and have more information on what owning a home costs.

In light of future trends that will impact the housing sector, getting finances ready will be essential in ensuring proper decision making. With being financially prepared, the process of owning a home will be easier.

At Reliance Financial, we suggest thar success in owning a home depends on two important aspects. First, the homeowner must meet the eligibility requirements for obtaining a mortgage loan. Secondly, he or she should be able to maintain financial records in the new home.

FAQs

What is the minimum credit score necessary to buy a house?

The vast majority of conventional mortgage lenders ask for a credit score greater than 620. However, people with credit scores over 740 can enjoy better terms, rates, and payments from lending institutions.

How important is debt-to-income ratio when qualifying for a mortgage?

This metric reflects what percentage of one’s income is used on monthly payments. This criterion is important when qualifying for a mortgage since the larger the debt-to-income ratio, the smaller the chances of obtaining a loan.

What are closing costs in the process of buying a house?

Closing costs refer to the additional payments made by the buyer at the final stages of home purchase. They include loan originations fees, title insurance, appraisal fees, tax charges, and many more. Closing costs represent between 2%-5% of the price of the home.

What type of mortgage loan should be chosen by first time homeowners?

First time homeowners normally choose FHA loan as a result of the smaller down payments and lower credit ratings required by such loans. However, selection of mortgage loan depends on various personal factors, including income and credit rating.

When should one prepare themselves financially for the purchase of a home?

One should prepare himself or herself two years before buying a home as it will assist in improving credit ratings, saving funds, and having sufficient finances for home purchase.