Purchasing a new home is one of the most significant financial milestones in life, but understanding how much income you need to qualify for a mortgage can be confusing. If you are considering a $500,000 mortgage, you are not alone; millions of prospective homebuyers are asking the same questions in today’s housing market. The answer isn’t simple, as it depends on several factors. While income plays a key role, lenders also consider your debt, down payment, and overall financial profile before approving a mortgage.

In this guide, we provide a simple explanation of how lenders calculate income requirements, what you may need to earn to qualify for a $500,000 mortgage, and how you can improve your chances of approval.

How Lenders Assess You?

When applying for a home loan, it is important to remember that lenders do not consider your income alone. Instead, they evaluate your overall financial situation based on several key factors:

Gross Income

This is your income before taxes and includes earnings from employment, such as your salary and bonuses. In addition to active income, lenders may also consider rental income and other verified sources.

Debt-to-Income Ratio (DTI)

One of the most important factors lenders consider is your DTI ratio. This is what lenders prefer more, which is the percentage of your income that goes towards paying off debts every month. In most cases, lenders find it acceptable if your DTI ratio is:

Front-end Ratio (only housing costs) is no more than 28% to 31% of your gross income.

Back-end Ratio (housing costs plus total debt payments) is no more than 36% to 43% of your gross income.

Credit Score

Lenders give you a loan based on your credit score. The higher the credit, the lower your interest rates will be. This will further lower the income you need to qualify for.

Down Payment Size

The size of your down payment directly affects the amount you can borrow and your monthly mortgage payments. A larger down payment reduces both your monthly payments and the income you need to qualify.

Estimating Your Monthly Mortgage Payment

To better understand your options, let us first estimate what your monthly payment might look like for a $500,000 mortgage. Your monthly payment typically includes the following components:

- Principal & Interest: This is the actual mortgage payment.

- Property Taxes: These vary by area but are usually estimated at 1% to 1.5% of the home’s value per year.

- Homeowners Insurance: Covers your home against damage or loss and is required by the lender.

- Private Mortgage Insurance (PMI): If you put down less than 20% on your home, then you will probably have to pay this until you have gained enough equity.

Using a 30-year fixed mortgage and today’s interest rates. Your principal and interest payment alone could be in the $3,000 to $3,700 per month range. When you factor in taxes and insurance, your total monthly housing expense could easily exceed $3,200 to $3,500+ per month. But remember, PMI is also the main factor, but if applicable.

Why is that important? Lenders are primarily concerned with how much you will be paying each month.

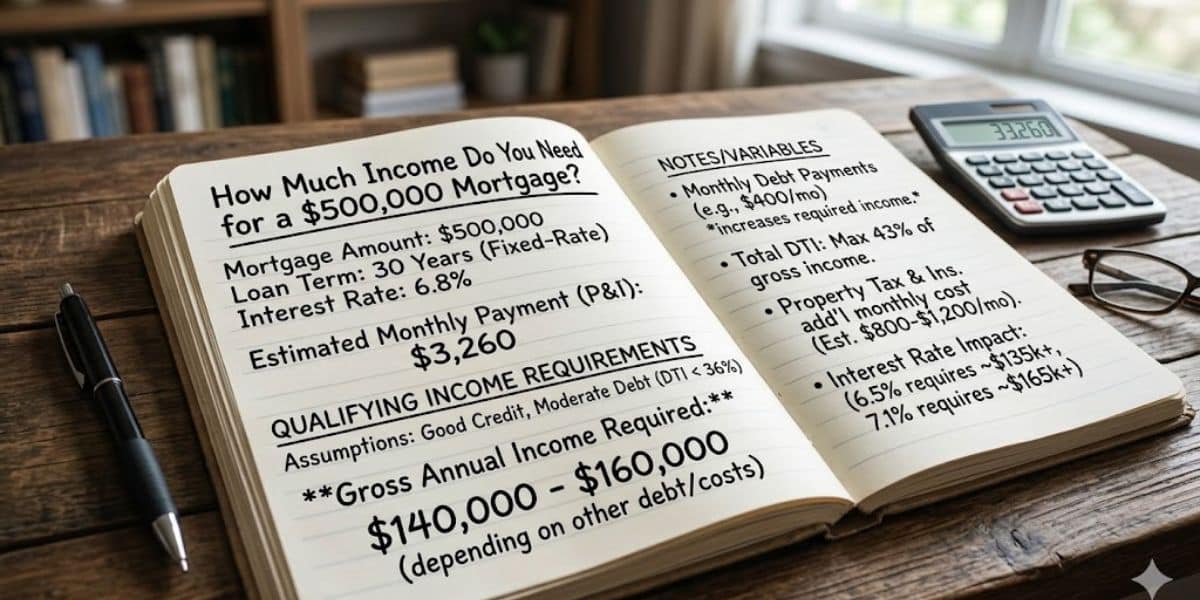

How Much Annual Income Do You Need?

To make calculations easier, mortgage affordability often uses the 28/36 rule:

- Front-end DTI (Housing Expenses): Should not exceed 28% of gross income.

- Back-end DTI (Housing Expenses + All Debt): Should not exceed 36% of gross income.

Using this rule, let us calculate the income required for a $500,000 mortgage.

Scenario: Estimated Monthly Housing Expense = $3,200

Front-end DTI:

Required gross monthly income= $3,200/0.28= $11,429

Required annual income= $11,429×12= $137,148

So, according to front-end DTI, you would need to earn approximately $137,000 per year.

Back end DTI:

If you have other monthly debt obligations (car loans, student loans, or credit cards, etc.), then your back-end DTI ratio should remain below 36%. For better understanding, if you have $500 in other monthly debt obligations:

Total monthly obligations= 3,200+500= 3,700

Required gross monthly income= 3,700/0.36= 10,278

Required annual income = 10,278 × 12 = $123,336

By this example, you would need to earn approximately $123,000 per year. Which is slightly lower than the front-end ratio. But remember that if your other monthly debt payments are higher than, then you would need to earn much more.

Higher Ratios (35/45 Rule)

Some mortgage programs allow slightly higher DTI ratios, such as 35% front end and 45% back end, especially for government-backed loans like FHA or VA. Using this guideline, a borrower would need to earn approximately $126,000 to $157,000 per year to qualify for a $500,000 mortgage.

How Down Payment Changes the Equation?

The difference your down payment makes is enormous when it comes to your income requirements:

20% Down Payment

With a 20% down payment ($100,000). Your loan amount will be reduced to $400,000. This means that:

- Your monthly mortgage payment will be lower

- The chances of needing to pay PMI will be lower

- The income you need to qualify for will be lower

In other words, your monthly payment will be several hundred dollars lower. This means that you may qualify for a lower income, which is potentially in the $110,000 to $130,000 range.

Smaller Down Payment

If you make a smaller down payment (5-10%), then you can expect:

- Higher monthly payments

- PMI

- Higher income requirements

Strategies to Qualify with Lower Income

If you are very close to qualifying but not quite there yet. Here we provide some strategies that you can use:

Save for a Larger Down Payment

A larger down payment reduces the amount you need to borrow and lowers the income required to qualify.

Pay Down Existing Debt

Paying down existing debt will help improve your debt-to-income ratio. Paying off a car loan or credit card debt can make a huge difference.

Improve Your Credit Score

Your credit score will determine your interest rate. A lower interest rate means a lower monthly payment and a lower income requirement.

Look into Other Loan Options

Government loans may have more flexible qualification requirements and income requirements. There are mainly FHA or VA loans.

Look into Co-Borrowing

If you are married or have a family member, then combining your income may help you qualify.

Final Thoughts

The actual income required for a $500,000 mortgage varies based on your personal financial profile and loan options. Most borrowers will require annual incomes ranging from $120,000 to $160,000. There are many factors, like lower debt and higher down payments, that play an important role. A good credit score will also work best to lower the required income.

At Reliance Financial, we have experts who understand your financial profile, and planning can certainly make the mortgage experience easier and more enjoyable. Whether you are purchasing your first home or upgrading to a $500,000 home. A reputable mortgage professional is required to make a stress-free journey.

FAQs about How Much Income You Need for a $500,000 Mortgage

What is the most important thing that lenders consider?

To qualify, lenders consider your income and credit history. There are also important factors like down payment and debt levels (as reflected by DTI ratios) to decide how much they can lend you. High income and low DTI are essential for approval.

Can I qualify for a mortgage with a lower income than these estimates?

Yes, it depends on your personal circumstances. You can qualify for a mortgage with a lower income if you have lower debt and high credit scores, along with large down payments.

How does my credit score impact income requirements?

A high credit score may qualify you for a lower interest rate, which will lower your monthly payment and make it easier to qualify for a mortgage with a lower income.

Do I need to make a 20% down payment to qualify for a mortgage?

No. You can qualify for a mortgage with a down payment of 3 to 5%. But remember, you will need to pay private mortgage insurance (PMI) until you have 20% equity in your home. A large down payment often translates to better terms and lower monthly payments.

Can I qualify for a mortgage with a co-borrower?

Yes, adding a co-borrower with income will improve your DTI ratio and make it easier to qualify for a larger mortgage.