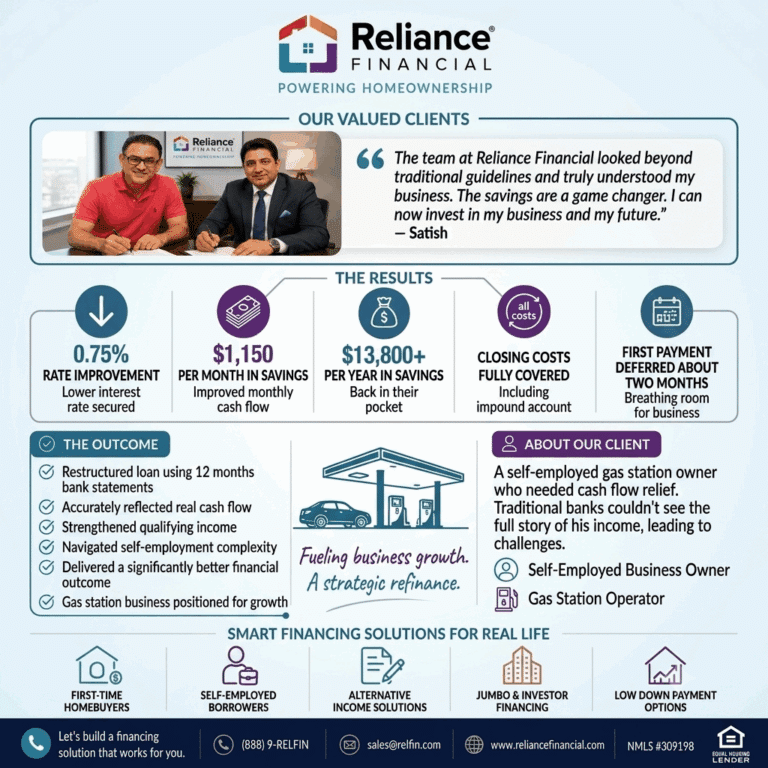

By restrategizing the loan using 12 months of bank statements and deposit analysis, Reliance Financial supported a self-employed business owner achieve a significantly better financial outcome during a tough economic period.

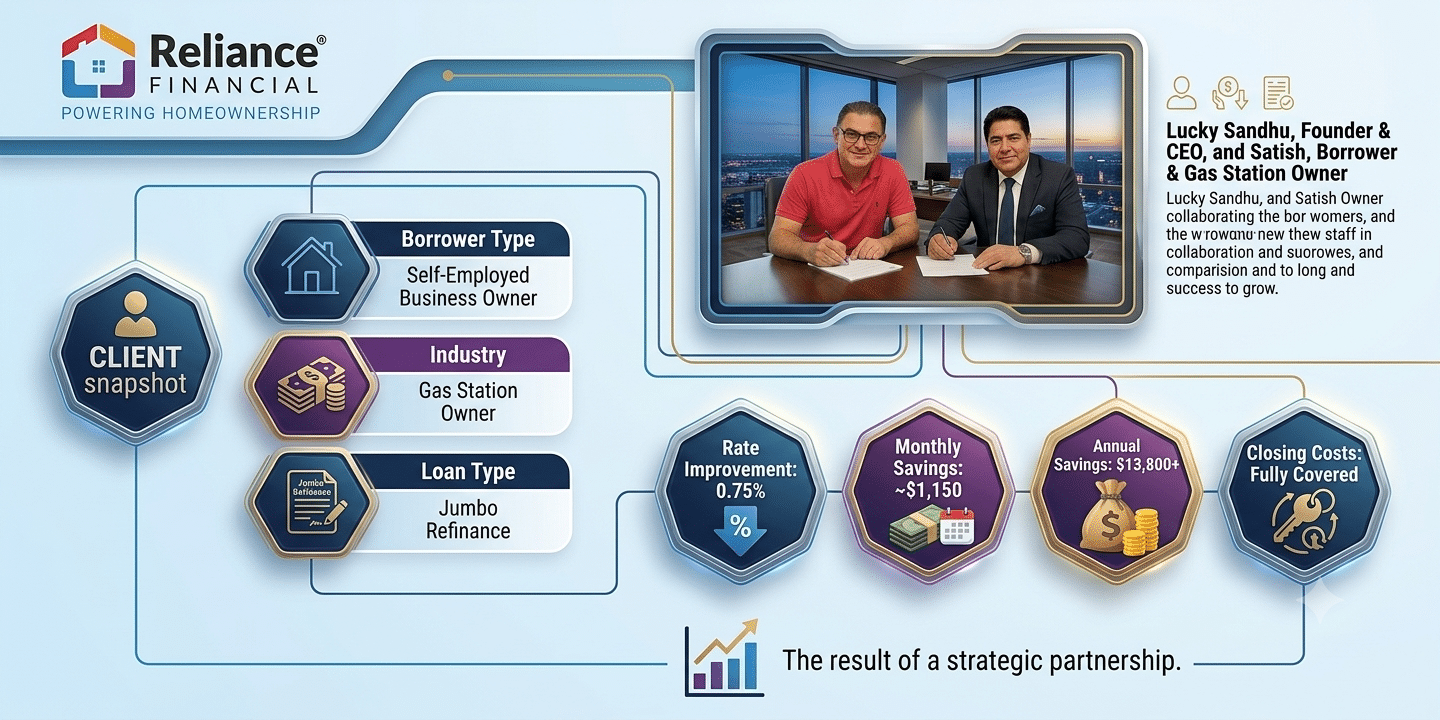

Client Snapshot

- Borrower Type: Self-Employed Business Owner

- Industry: Gas Station Owner

- Loan Type: Jumbo Refinance

- Loan-to-Value (LTV): 65%

- Income Qualification Method: 12-Month Bank Statements

- Rate Improvement: 0.75%

- Monthly Savings: Approximately $1,150

- Annual Savings: Over $13,800

- Closing Costs: Fully Covered

- Impound Account: Paid Through Loan Structure

- First Mortgage Payment Deferred Approximately Two Months Through Loan Structuring

Why Traditional Lending Fell Short

Many traditional lenders rely heavily on tax return income when evaluating self-employed borrowers.

However, tax returns often do not fully reflect the true cash flow and financial strength of business owners who strategically manage deductions, expenses, and reinvestment into their companies.

As a result, many qualified self-employed borrowers are underserved by conventional underwriting approaches.

The Challenge

The borrower owned and operated a gas station business and, like many small business owners, was navigating increased cash flow pressure due to rising fuel prices and broader economic uncertainty tied to geopolitical events in the Middle East.

Although the borrower had a strong business and consistent deposits, traditional income calculations based primarily on tax returns significantly limited the available refinancing options.

The borrower needed:

- improved monthly cash flow

- reduced financial pressure

- a smarter financing structure

- and a lender that understood self-employment complexity

The Reliance Financial Strategy

Reliance Financial structured a customized jumbo refinance solution designed around the borrower’s real-world cash flow rather than relying solely on traditional tax return calculations.

Key elements of the strategy included:

12-Month Bank Statement Analysis

The loan was structured using 12 months of verified bank statements and deposit analysis to present a more accurate picture of the borrower’s income and cash flow.

Improved Jumbo Financing Structure

By restructuring the file strategically, Reliance Financial secured a significantly improved interest rate for the borrower.

0.75% Lower Interest Rate

The refinance delivered approximately a 0.75% rate improvement compared to the borrower’s previous financing structure.

Meaningful Monthly Savings

The borrower reduced their monthly mortgage obligation by approximately $1,150 per month.

Over $13,800 in Annual Savings

The refinance created substantial long-term cash flow improvement and financial flexibility.

Closing Costs Fully Covered

Reliance Financial structured the transaction to cover all closing costs, including the borrower’s impound account.

Additional Payment Relief

Through a slightly higher loan amount structure, one mortgage payment was effectively covered, allowing the borrower approximately two months before making their first post-refinance mortgage payment.

This created valuable breathing room for the borrower to stabilize and strengthen business cash flow during a challenging period.

The Outcome

The result was not simply a refinance.

It was a strategic financial reset.

Final Results

- Approximately $1,150/month in savings

- Over $13,800/year in improved cash flow

- 75% lower interest rate

- No out-of-pocket closing costs

- Impound account fully covered

- Additional short-term payment relief created

- Improved financial flexibility for the business owner

- Capital preserved for future investments and opportunities

The borrower was especially excited about redirecting the savings toward higher-yielding investment opportunities and strengthening long-term financial positioning.

Same Borrower. Same Property. Completely Different Outcome.

This transaction demonstrates how the right loan structure can dramatically change a borrower’s financial outcome.

When approached strategically, alternative income analysis and customized financing solutions may create opportunities that traditional underwriting methods often overlook.

What Borrowers Can Learn

Many self-employed borrowers assume refinancing options are limited if tax returns do not fully reflect business cash flow.

However, specialized programs such as bank statement loans may allow lenders to evaluate income differently by analyzing verified deposits and real operating cash flow.

For the right borrower profile, strategic loan structuring can:

- improve monthly cash flow

- preserve liquidity

- reduce financial pressure

- and create stronger long-term financial flexibility

Smart Financing Solutions for Self-Employed Borrowers

Reliance Financial specializes in helping:

- Self-Employed Borrowers

- Business Owners

- Jumbo Loan Clients

- Alternative Income Borrowers

- Real Estate Investors

- High-Income Professionals

Recent Posts

Categories