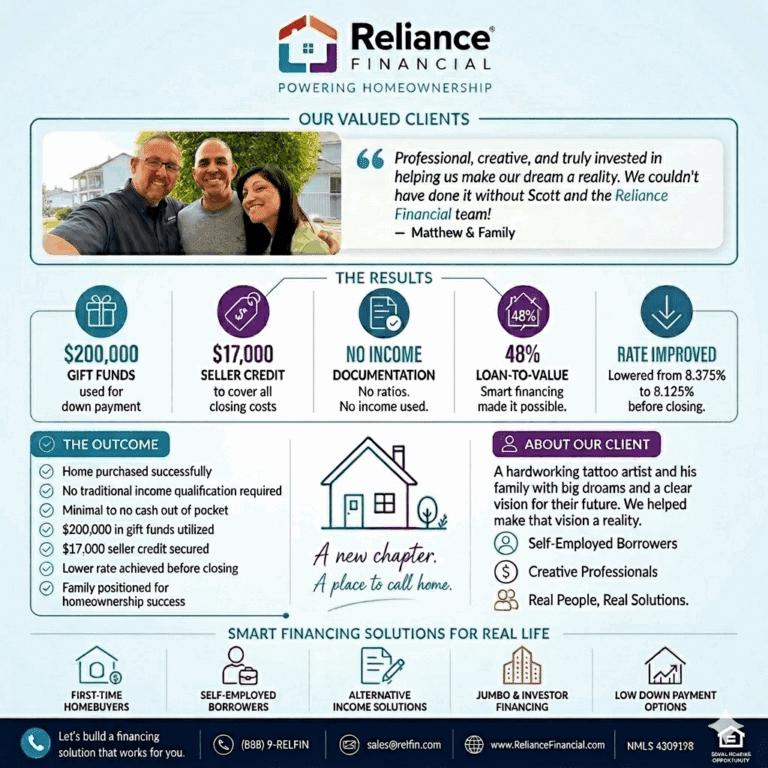

Creative financing and smart strategy along with a people first approach helped Mathew and his family get homeownership with the help of a tailored mortgage solution specifically designed outside traditional lending guidelines.

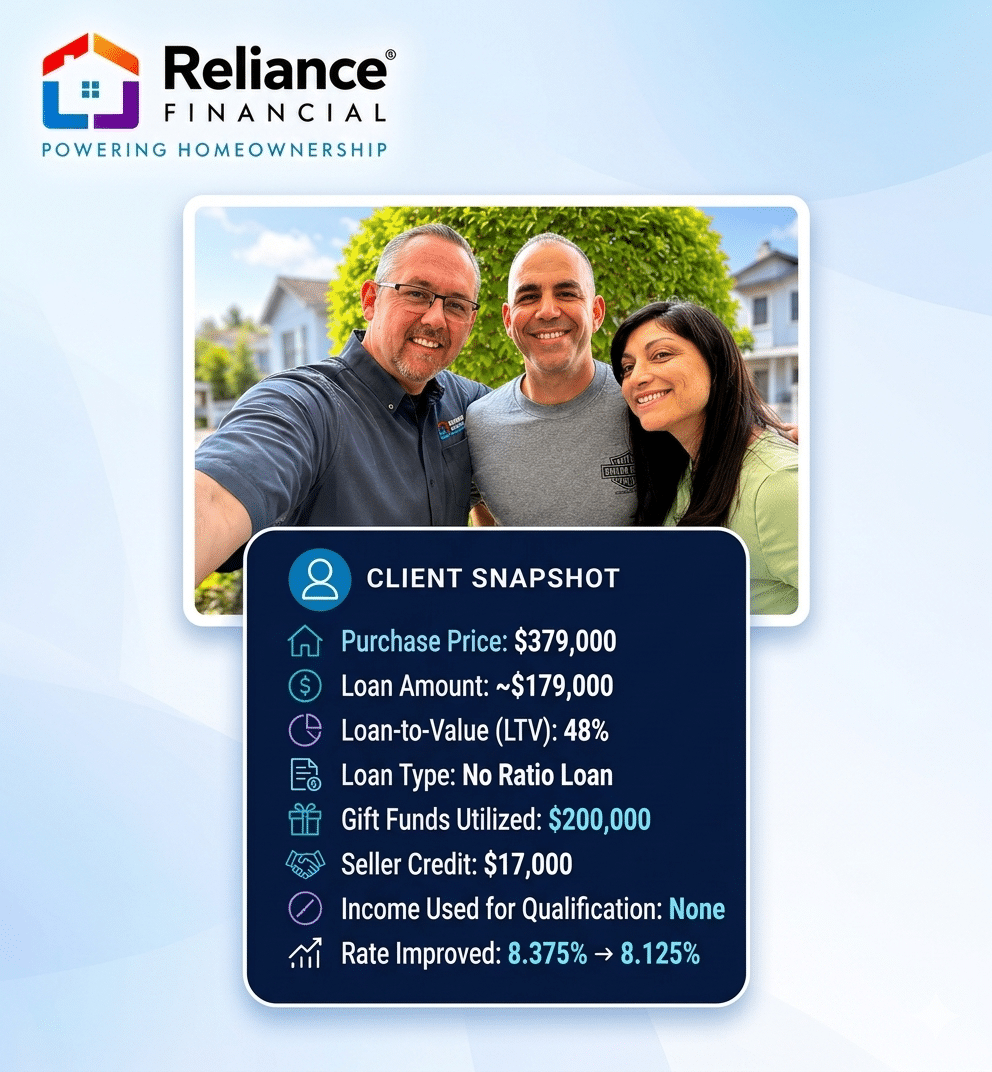

Client Snapshot

- Borrower Type: Self-Employed Tattoo Artist

- Purchase Price: $379,000

- Loan Amount: Approximately $179,000

- Loan-to-Value (LTV): 48%

- Loan Type: No Ratio Mortgage Loan

- Gift Funds Utilized: $200,000

- Seller Credit Negotiated: $17,000

- Income Used for Qualification: None

- Final Rate Improvement: 8.375% → 8.125%

chapter in life.

Why Traditional Financing Wasn’t the Right Fit?

A lot of banks and traditional lenders depend purely on strict income documentation formulas that may not properly showcase the financial strength of self-employed professionals, business owners and commission based borrowers.

For borrowers who are looking for mortgage options without traditional tax return qualification, getting the right financing strategy mostly needs a more tailors and solution specific approach.

That’s where the team at Reliance Financial, led by Scott Wise, Head of Mortgage Loan Production, stepped in. With the help of creative non-QM mortgage solution, the family was able to pursue homeownership with the help of a financing structure specially made for borrowers with non-traditional income profiles.

The Challenge

Like other self-employed borrowers, Matthew and his family had their doubts that traditional mortgage financing does not always help in solving the problem.

The family had a strong overall financial support and a clear road to homeownership but they faced challenge with documenting income via conventional lending guidelines with traditional lenders.

As business owners and creators most of the time find out, getting qualified for a home loan without depending heavily on traditional tax return can become difficult via standard bank financing procedures.

Simultaneously, preserving liquidity and lowering upfront cash needs were crucial priorities for the family because they were getting ready for this next chapter in life.

The Reliance Financial Strategy

The team of Reliance Financial worked closely with the family and Realtor to strategize a tailored mortgage solution customized to their specific financial situation.

No Ratio Non-QM Loan Structure

The loan was approved using a no ratio non-QM mortgage program. This means traditional income calculations were not required for qualification.

For many self-employed borrowers, business owners and creators, alternative income mortgage solutions such as non-QM loans may provide financing flexibility outside conventional guidelines.

$200,000 in Gift Funds

The borrowers were able to utilize approximately $200,000 in gift funds toward the down payment.

$17,000 Seller Credit Negotiated

Their Realtor successfully negotiated approximately $17,000 in seller credits to help offset closing costs.

Seller credits can significantly reduce upfront cash-to-close requirements for qualified homebuyers.

Minimal Cash Out of Pocket

By combining the gift funds and seller credits strategically, the borrowers were able to complete the transaction with little to no cash contribution of their own.

Last-Minute Rate Improvement

Just before closing, Scott Wise was able to get a rate exception and improve the interest rate from 8.375% down to 8.125%, helping create additional long-term savings for the family.

The Outcome

Through a combination of creative financing, strategic loan structuring, and our experienced teamwork, Matthew and his family were able to successfully purchase their home with minimal borrower funds required at closing.

Final Results

- Home purchased successfully

- No traditional income qualification required

- Minimal borrower cash contribution

- $200,000 in gift funds utilized

- $17,000 seller credit secured

- Improved interest rate before closing

- Family positioned for long-term

- homeownership success

A Relationship-Driven Experience

One of the most rewarding aspects of this transaction was the relationship built throughout the process.

The tattoo artist community is highly connected and relationship-driven, and the experience created meaningful trust between the family and the Reliance Financial team.

Because of the financing solution and overall experience, Matthew has already begun referring coworkers, peers, and others within the tattoo artist community who may also need creative financing solutions outside traditional lending guidelines.

At Reliance Financial, we believe great mortgage experiences naturally create long-term relationships, referrals, and trust.

What Borrowers Can Learn

Many self-employed borrowers assume they cannot qualify for financing if their income situation falls outside traditional lending guidelines.

However, specialized mortgage programs such as no ratio loans and non-QM mortgage solutions may provide alternative paths to homeownership for certain borrowers, particularly:

- Self-employed professionals

- Entrepreneurs

- Artists and creators

- Business owners

- Commission-based professionals

Gift funds and seller credits may also help reduce upfront cash requirements depending on the borrower profile and loan structure.

For borrowers wondering how to buy a home when self-employed or searching for mortgage options without traditional tax returns, working with a lender experienced in alternative income mortgage programs can make a meaningful difference.

Looking for Creative Mortgage Solutions?

At Reliance Financial we specialize in helping:

- First-time homebuyers

- Self-employed borrowers

- Entrepreneurs and creators

- Real estate investors

- Jumbo loan clients

- Alternative income borrowers

- Non-QM mortgage clients

Whether you’re purchasing, refinancing, or exploring your options, our team works to structure financing solutions tailored to your unique goals.

Recent Posts

Categories