Are you in the market to buy a new home or perhaps considering a mortgage refinance? Chances are you have come across a term that sounds unfamiliar and a little intimidating: mortgage points. But what exactly are mortgage points? How do mortgage points impact interest rates and mortgage payments? And perhaps the most important question of all – should you ever pay mortgage points?

In this ultimate guide, we will cover everything you need to know about mortgage points:

- What are they?

- How do they work?

- Whether or not you should pay for them?

Understanding the Basics: What Are Mortgage Points?

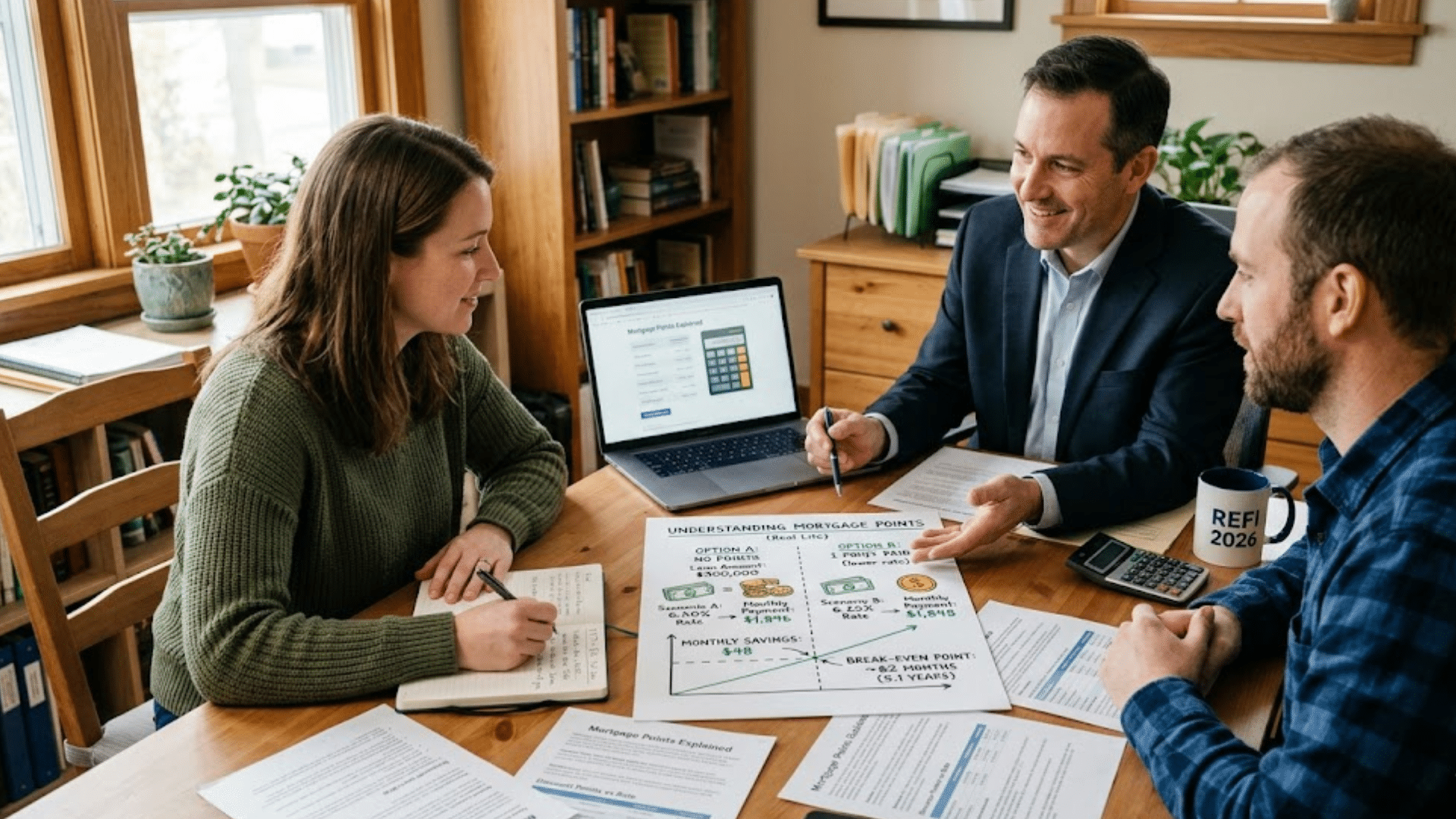

Mortgage points, also known as discount points are fees that borrowers pay in order to lower the interest rate on their mortgage. One mortgage point is usually 1% of the total mortgage amount. For example, if you are borrowing $300,000 to buy a house, one mortgage point will cost you $3,000.

The process of purchasing mortgage points is akin to prepaying interest on your mortgage. Instead of paying a slightly higher interest rate over the course of your loan, you pay a lump sum upfront to lower the interest rate for its entire term. This can save you a great deal in the long run.

Mortgage Points vs Origination Points

Below are the two terms that are often used:

| Type of Point | Purpose | Impact on Interest |

| Discount Points (Mortgage Points) | Prepay interest to lower your rate | Yes — Reduces the interest rate |

| Origination Points | Fees paid to the lender to originate the loan | No — Does not reduce the interest rate |

Origination points are fees charged to the borrower by the lender to process the mortgage. These points have no effect on the interest rate. Remember discount points are used to lower the mortgage rate.

How Do Mortgage Points Work?

When your lender presents you with a mortgage offer, you will see rates with and without points. If you opt to purchase points, then you will pay them at closing. This will give you a lower interest rate. This reduction is normally 0.25% per point. However, the rate reduction can vary depending on the market and the lender.

- 1 point = 1% of your loan amount

- Typical reduction in interest rate = 0.25% per point

- You pay points at closing as part of your upfront costs

Let’s understand with an example for better clarity: If you are buying a home worth $400,000 and your points amount to $4,000 (which is 1 point), then you will pay $4,000 at closing. This could lower your interest rate from 6.50% to 6.25%. This can mean savings of hundreds or even thousands of dollars.

The Break-Even Point: Is It Worth Buying Points?

The break-even point is one of the most critical factors to consider when evaluating mortgage points because it determines how many months it will take to recover the cost of the points.

Quick instruction on how to calculate the break-even point:

- Break-even = Cost of points ÷ Monthly savings

Let’s use an example to illustrate the calculation:

Suppose you’re planning to buy discount points that cost $2,000, and you save $50 each month on your mortgage payments as a result. In that case, the break-even point will be 40 months ($2,000 divided by $50). As a result, if you plan to stay in that house for more than 40 months, you’ll benefit from the points you paid for.

However, if you plan to sell the house or refinance it within that period, you may never benefit from the points you paid. This is one of the reasons mortgage points are more advantageous if you plan to stay in that house for a long time.

Example: How Mortgage Points Affect Your Loan

Let’s use an example to show how mortgage points can affect the cost of the loan. Assume that you are borrowing $350,000 for a 30-year term:

| Option | Interest Rate | Monthly Payment | Total Interest |

| No Points | 6.50% | $2,212.24 | $446,404.28 |

| 1 Point ($3,500) | 6.25% | $2,155.01 | $425,803.81 |

| 2 Points ($7,000) | 6.00% | $2,098.43 | $405,431.62 |

In this example, purchasing points reduces both the monthly payment and the total amount of interest you will pay. As shown above, buying two points saves you more than $40,000 in interest. However, you must consider whether paying the additional $7,000 upfront is worth it.

Partial Points and Seller Contributions

Not all lenders restrict you to whole points. Many lenders offer the option to purchase partial points – for example, half a point for a reduced cost and a smaller rate reduction.

Seller contributions toward mortgage points are sometimes part of home purchase negotiations. This can be a useful tactic to help the buyer reduce the overall interest cost of the loan without paying the full amount themselves.

Pros and Cons of Buying Mortgage Points

Pros

- Less expensive monthly payments: A lower interest rate means lower payments

- Less interest paid: You pay less interest over the life of your mortgage

Cons

- Higher upfront costs: You are essentially buying points, which can be difficult if you’re already stretching to cover the down payment.

- Break-even time requirement: You need to stay in your house long enough to recover the cost of the points.

- Not ideal for short-term ownership: If you plan to sell your house within a few years, buying points may not make sense.

When Should You Consider Buying Mortgage Points?

There are certain situations where you may want to consider buying mortgage points. These include:

- If you plan to stay in your home for a long time

- If you want to minimize your mortgage payments

- If you have spare funds after making the down payment

- If interest rates are high and any reduction would be beneficial

You may not need to consider buying mortgage points under the following situations:

- If you plan to refinance your mortgage

- If you prefer to use the funds for other objectives

Conclusion

With mortgage points, a borrower is able to lower the interest rate by making a payment at closing. This can end up saving thousands of dollars down the road. For more go through Reliance Financial. While this is a great option, it is not always the best choice. So, carefully examine the:

- Break-even point

- Long-term goals

- Financial objectives

FAQs About What Are Mortgage Points & How Do They Work

How much does one mortgage point save me on my mortgage payments?

Generally speaking, one mortgage point can reduce your interest rate by around 0.25%. However, the actual savings may vary depending on the lender and market conditions.

Are mortgage points tax-deductible?

Generally speaking, yes – discount points may be tax-deductible under the Internal Revenue Service rules on home mortgage interest. However, you should consult a professional tax advisor for guidance.

When is buying mortgage points a good idea?

Mortgage points can be a good idea if you plan to stay in the home long enough to benefit from the interest savings.

Can I buy partial mortgage points?

Yes, many lenders allow you to purchase partial points, such as 0.5 points, depending on their terms.